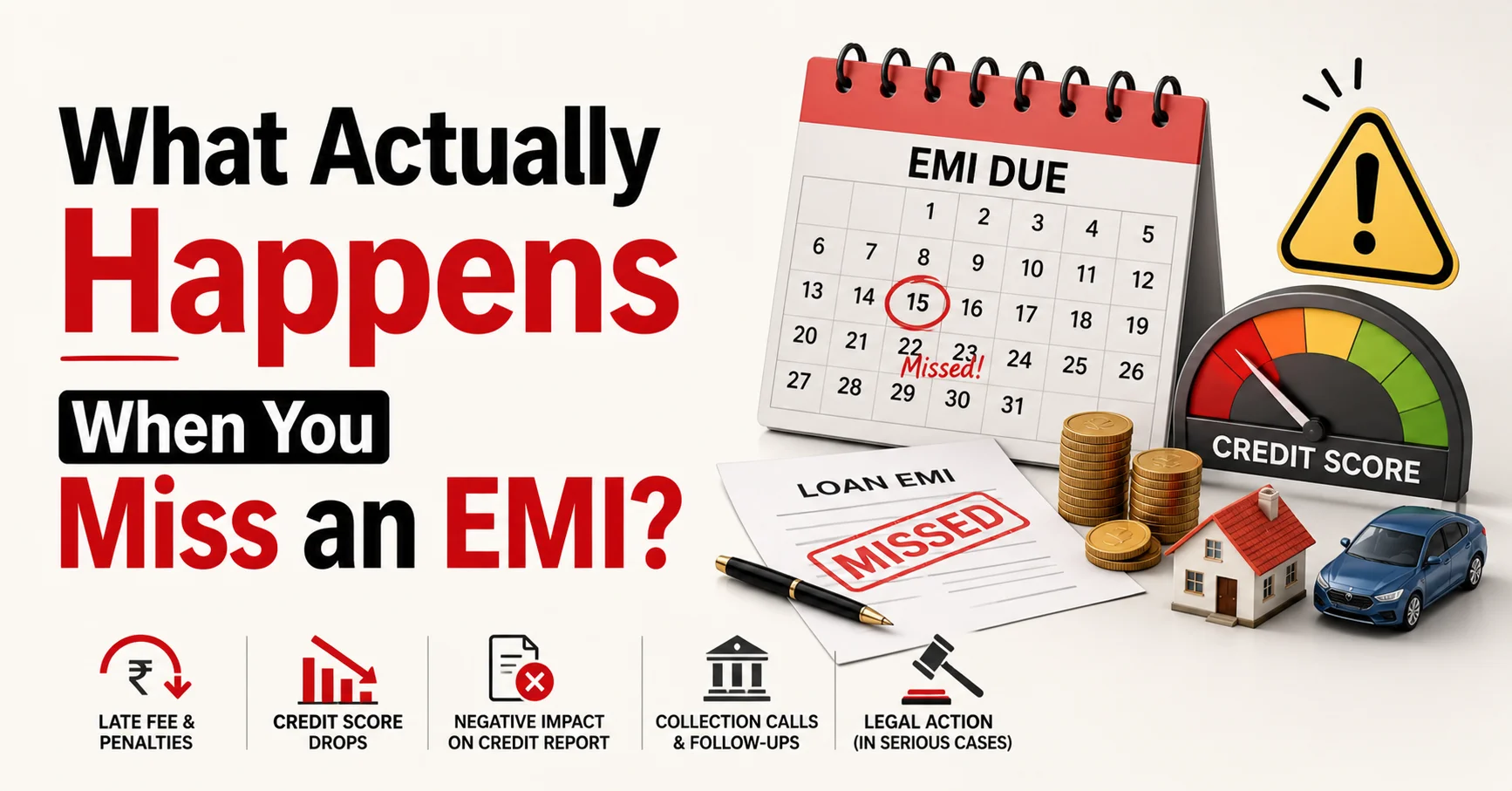

Missing an EMI (Equated Monthly Installment) can feel stressful, but understanding what actually happens helps you handle the situation better. Whether it’s a personal loan, home loan, or credit card EMI, the consequences follow a clear pattern.

Let’s break it down in simple terms.

What is an EMI?

An EMI is a fixed monthly payment you make to repay a loan. It includes:

- Principal amount

- Interest

Banks and NBFCs (Non-Banking Financial Companies) expect you to pay it on time every month.

What Happens If You Miss an EMI?

1. Immediate Late Payment Penalty

As soon as you miss your EMI:

👉 The lender charges a late fee or penalty

- Usually 1%–3% of EMI amount

- Sometimes a fixed charge

This increases your total repayment amount.

2. Negative Impact on Credit Score

Your credit score is tracked by agencies like CIBIL.

👉 Missing even one EMI can:

- Lower your credit score

- Stay on your report for years

Why this matters:

- Future loans become harder

- Higher interest rates

- Credit card approvals may get rejected

3. Reminder Calls & Messages

After missing EMI:

- You’ll get SMS alerts

- Calls from the bank

- Email reminders

👉 This is the early stage—no legal action yet.

4. EMI Becomes “Overdue”

If not paid within a few days:

👉 Your EMI is marked as overdue

This status is reported to credit bureaus like TransUnion CIBIL.

5. Multiple Missed EMIs = Serious Trouble

If you miss EMIs for 2–3 months:

- Penalties keep increasing

- Credit score drops heavily

- Collection agents may contact you

6. Loan Account Becomes NPA

If you don’t pay for 90 days (3 months):

👉 Your loan is classified as:

Non-Performing Asset

What this means:

- Serious default

- Strong legal action can begin

- Your financial reputation is damaged

7. Legal Action or Recovery Process

In extreme cases:

- Legal notices may be sent

- Recovery agents may visit

- Assets (like car/home) can be seized

👉 Especially in secured loans like:

- Home loans

- Car loans

Real-Life Example

Let’s say your EMI = ₹10,000

- Miss 1 EMI → Pay ₹10,000 + penalty

- Miss 2–3 EMIs → Heavy penalties + credit damage

- Miss 3+ months → Risk of legal action

Common Mistakes People Make

❌ Ignoring the problem

👉 It gets worse over time

❌ Not talking to the bank

👉 Banks often offer solutions

❌ Taking more loans to repay old ones

👉 This creates a debt trap

What Should You Do If You Miss an EMI?

1. Pay As Soon As Possible

Even a delayed payment is better than no payment.

2. Talk to Your Lender

Banks may offer:

- Grace period

- EMI restructuring

- Temporary relief

3. Use Emergency Funds

If possible, use savings to avoid long-term damage.

4. Enable Auto-Debit

Avoid missing future EMIs by setting up auto payments.

5. Plan Your Budget Better

Track income and expenses to stay on track.

Pro Tips to Avoid Missing EMI

- Keep a buffer amount in your account

- Set payment reminders

- Avoid taking loans beyond your capacity

- Maintain an emergency fund (3–6 months expenses)

Impact Summary

| Situation | Impact |

|---|---|

| 1 missed EMI | Small penalty + slight credit drop |

| 2–3 missed EMIs | High penalty + major credit impact |

| 90+ days delay | NPA + legal risk |

Conclusion

Missing an EMI once is not the end of the world—but ignoring it can lead to serious financial problems. From penalties and credit score damage to legal action, the consequences grow over time.

👉 The best approach is simple:

- Pay on time

- Act quickly if missed

- Stay financially disciplined

FAQs

1. What happens if I miss one EMI?

You will be charged a penalty and your credit score may drop slightly.

2. Will missing EMI affect my credit score?

Yes, it is reported to CIBIL and can lower your score.

3. How many EMIs can I miss before legal action?

Usually after 3 months (90 days) of non-payment, legal action may start.

4. Can I go to jail for missing EMI?

No, but legal recovery actions can be taken.

5. Can I recover my credit score after missing EMI?

Yes, by paying dues on time and maintaining good credit behavior.

Also Read: How to Track Daily Expenses in Excel Mobile (Step-by-Step Guide)