Car insurance can be confusing, especially with terms like “bumper-to-bumper” or “zero depreciation cover.” Many vehicle owners assume they have full coverage, only to discover limitations during a claim.

If you want to be sure about your policy, this guide will help you check whether your insurance is truly bumper-to-bumper and what it actually covers.

What is Bumper-to-Bumper Insurance?

Bumper-to-bumper insurance, also known as zero depreciation cover, is an add-on to your standard car insurance policy. It ensures that no depreciation is deducted during claim settlement.

This means:

- You get the full cost of replacing damaged parts

- No deduction for wear and tear

- Higher claim amount compared to regular insurance

Why It Matters

In standard insurance:

- Plastic, rubber, and metal parts undergo depreciation

- You may receive 50% or less of the claim value

With bumper-to-bumper insurance:

- You get almost 100% claim settlement (excluding deductibles)

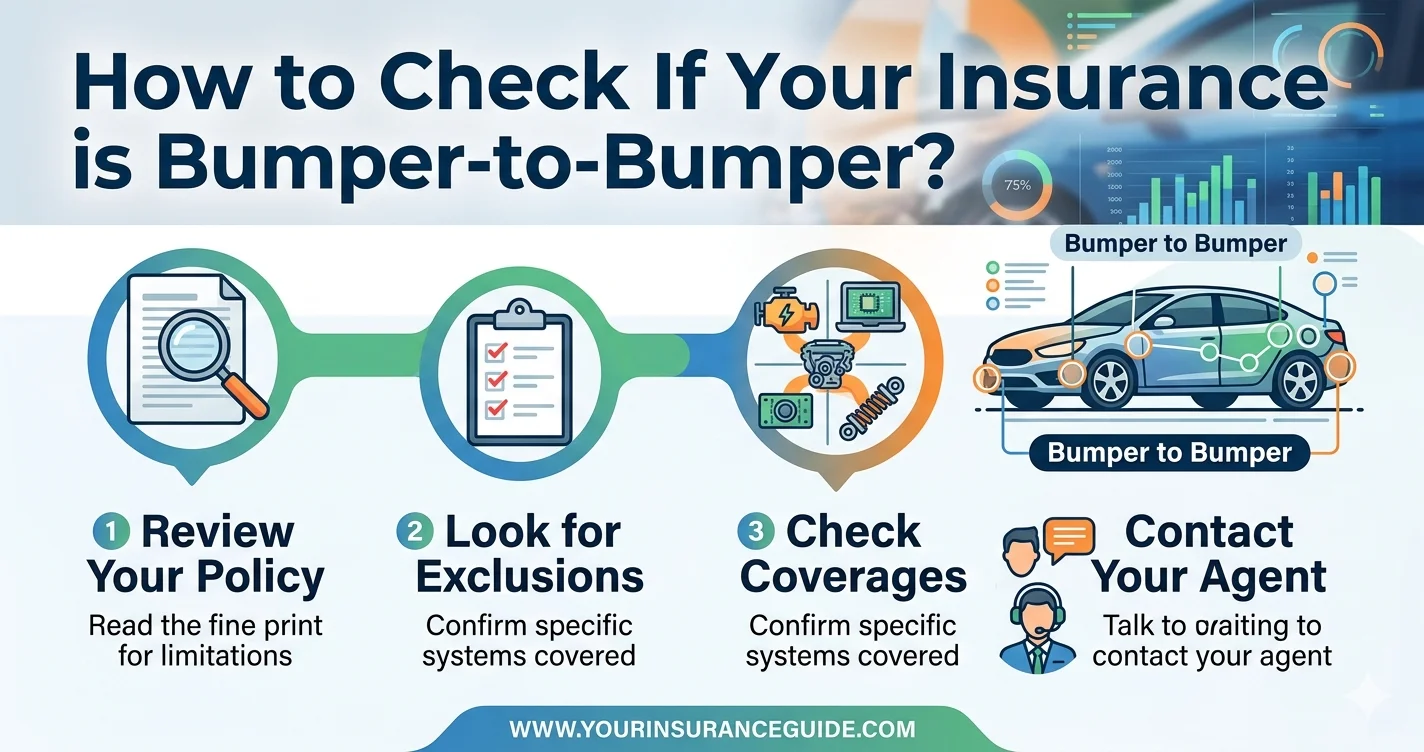

How to Check If Your Insurance is Bumper-to-Bumper

1. Review Your Policy Document

The easiest way is to check your policy document.

Look for terms like:

- “Zero Depreciation Cover”

- “Nil Depreciation”

- “Bumper-to-Bumper Add-on”

If these are mentioned, your policy includes this coverage.

2. Check the Add-Ons Section

Bumper-to-bumper is not included by default—it’s an add-on.

Go to:

- Add-ons or riders section

- Coverage details

If it’s listed there, you’re covered.

3. Log in to Your Insurance Account

Most insurers provide online dashboards.

Steps:

- Log in to your insurer’s website or app

- Open your policy details

- Check add-ons and benefits

4. Contact Customer Support

If you’re unsure, call or email your insurer.

Ask directly:

- “Do I have zero depreciation cover in my policy?”

5. Check Your Premium Amount

Bumper-to-bumper insurance costs more than regular policies.

If your premium is slightly higher, it may include:

- Zero depreciation

- Additional add-ons

What Does Bumper-to-Bumper Insurance Cover?

- Full cost of damaged parts

- Plastic and fiber components

- Rubber parts

- Metal parts without depreciation

What It Does NOT Cover

- Engine damage due to negligence

- Driving without a valid license

- Regular wear and tear (non-accidental)

- Mechanical breakdown

Always read the fine print for exclusions.

Benefits of Bumper-to-Bumper Insurance

1. Higher Claim Amount

You get maximum reimbursement with minimal deductions.

2. Peace of Mind

No surprises during claim settlement.

3. Ideal for New Cars

Best suited for vehicles less than 5 years old.

4. Saves Out-of-Pocket Expenses

Reduces the amount you pay during repairs.

Tips Before Buying or Renewing

- Always opt for zero depreciation for new cars

- Compare policies from different insurers

- Read terms carefully

- Check claim limits (some policies allow limited claims per year)

Common Mistakes to Avoid

- Assuming it’s included by default

- Not reading policy documents

- Ignoring add-on details

- Choosing cheapest policy without coverage

Conclusion

Bumper-to-bumper insurance offers one of the most comprehensive protections for your car. However, since it’s an add-on, you must verify its inclusion in your policy.

By reviewing your policy documents, checking add-ons, and confirming with your insurer, you can ensure that you’re fully protected when it matters most.

A small step today can save you significant money and stress during a claim.

FAQs

1. Is bumper-to-bumper insurance the same as zero depreciation?

Yes, both terms are used interchangeably.

2. Is it included in all car insurance policies?

No, it is an add-on and must be selected separately.

3. How much does it cost?

It usually increases your premium by 10–20%.

4. Is it worth it for old cars?

It’s most beneficial for cars under 5 years old.

5. Can I add it during renewal?

Yes, you can include zero depreciation cover while renewing your policy.

Also Read: Best Buy 101: Best Passenger Tire