Your 20s are one of the most important decades of your life—not just for your career, but also for your financial future. The habits you build during this time can either set you up for long-term success or create financial stress later.

In India, where expenses are rising and lifestyle choices are changing rapidly, learning how to manage money early is more important than ever. Whether you are a student, a fresher, or a young professional, this guide will help you understand how to take control of your finances in your 20s.

Why Money Management in Your 20s is Important

Most people start earning in their early 20s but often lack financial planning. Without proper money management, it’s easy to fall into habits like overspending, saving less, or relying on credit.

Managing money early helps you:

- Build strong financial habits

- Avoid debt traps

- Save and invest wisely

- Achieve long-term financial goals

👉 The earlier you start, the easier your financial journey becomes.

Step 1: Understand Your Income and Expenses

The first step in money management is awareness.

Track:

- Your monthly income

- Fixed expenses (rent, bills)

- Variable expenses (food, shopping, travel)

👉 Many people don’t realize where their money goes.

Once you track your spending, you can:

- Identify unnecessary expenses

- Control your budget

- Improve savings

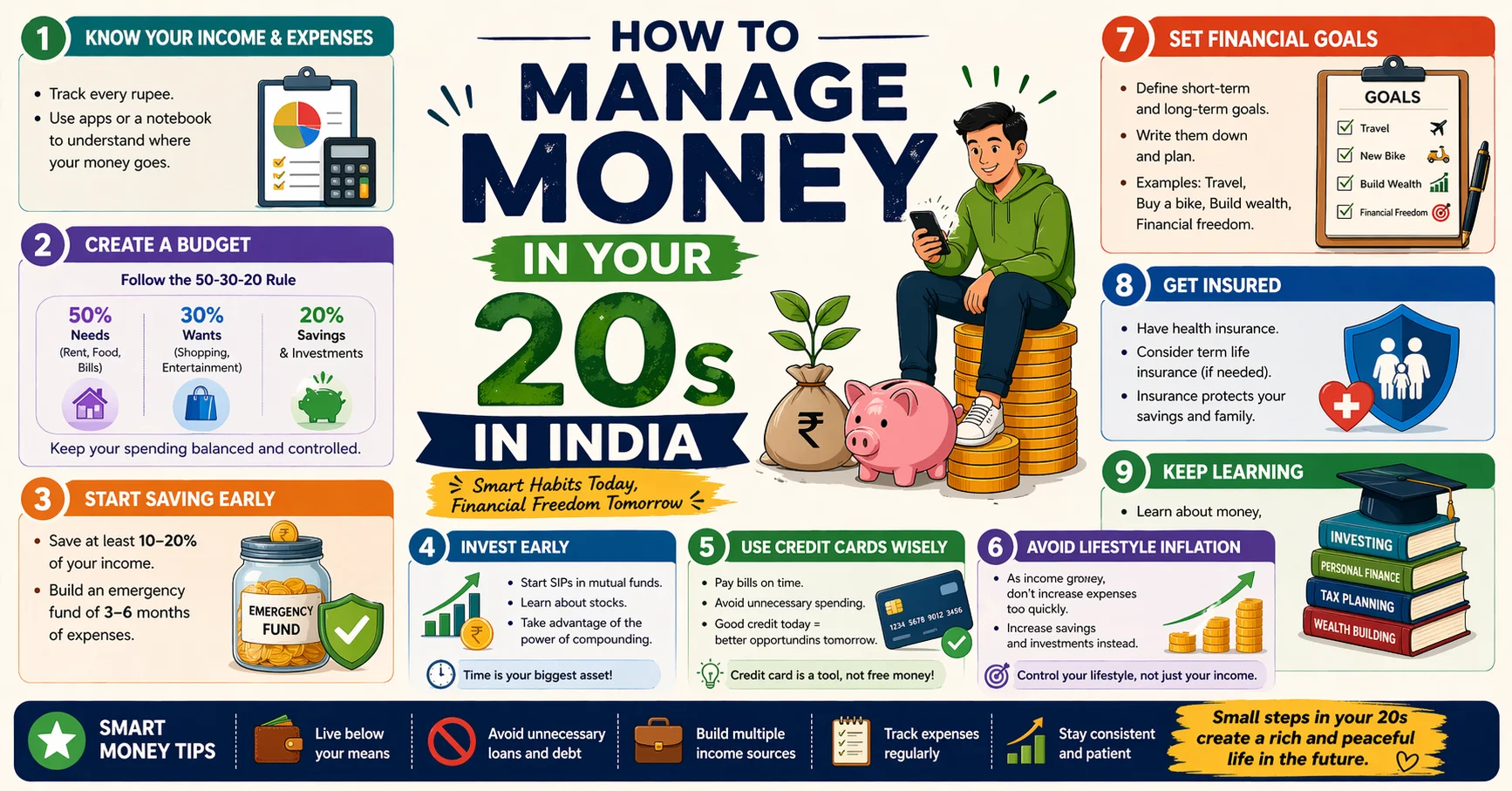

Step 2: Create a Monthly Budget

Budgeting is the foundation of financial success.

One simple method is the 50-30-20 rule:

- 50% for needs (rent, food, bills)

- 30% for wants (shopping, entertainment)

- 20% for savings

👉 This keeps your spending balanced and controlled.

Step 3: Start Saving Early

Saving should be your priority, not an afterthought.

Even if you earn a small amount:

👉 Save at least 10–20% of your income

Start with:

- Emergency fund

- Short-term savings

🧾 Emergency Fund

Build a fund that covers:

👉 3–6 months of expenses

This helps during:

- Job loss

- Medical emergencies

- Unexpected expenses

Step 4: Start Investing Early

One of the biggest advantages in your 20s is time.

👉 The earlier you invest, the more your money grows

You can start with:

- Mutual funds

- SIPs (Systematic Investment Plans)

- Stocks (after learning basics)

🔄 Power of Compounding

When you invest early:

👉 Your money earns returns

👉 Those returns also earn returns

This leads to exponential growth over time.

Step 5: Use Credit Cards Wisely

Credit cards can be helpful if used properly.

✔ Pay full bill on time

✔ Avoid unnecessary spending

✔ Use for planned expenses only

❌ Don’t:

- Overspend

- Miss payments

👉 Misuse can lead to debt traps

Step 6: Avoid Lifestyle Inflation

As income increases, many people increase their spending.

This is called:

👉 Lifestyle inflation

Instead:

- Increase savings

- Invest more

👉 Control your lifestyle, not just your income

Step 7: Set Financial Goals

Having clear goals helps you stay focused.

Examples:

- Buy a bike

- Travel

- Build savings

- Invest for future

Divide goals into:

- Short-term (1–2 years)

- Long-term (5–10 years)

Step 8: Track Your Expenses Regularly

Tracking helps you:

- Stay aware

- Avoid overspending

- Improve budgeting

👉 Even small daily expenses matter

Step 9: Learn Basic Financial Skills

You don’t need to be an expert, but basic knowledge is important.

Learn about:

- Saving

- Investing

- Taxes

- Insurance

👉 Financial knowledge = financial power

Step 10: Get Insurance Early

Many people ignore insurance in their 20s.

But it’s important to have:

- Health insurance

- Basic life insurance (if needed)

👉 It protects you from unexpected financial risks

Smart Money Tips for Your 20s (India)

✔ Live Below Your Means

Spend less than you earn

✔ Avoid Unnecessary Loans

Only take loans when necessary

✔ Build Multiple Income Sources

Side income helps grow wealth faster

✔ Invest in Yourself

Learn new skills to increase earning potential

✔ Stay Consistent

Consistency matters more than amount

Common Money Mistakes to Avoid

- Not saving at all

- Spending on unnecessary things

- Ignoring investments

- Taking too much debt

- Not tracking expenses

👉 Avoiding these mistakes can save you years of financial stress

Example Monthly Budget (India)

| Category | Percentage |

|---|---|

| Needs | 50% |

| Wants | 30% |

| Savings | 20% |

Final Thoughts

Your 20s are the best time to build a strong financial foundation. You don’t need a high salary to start managing money—you just need the right habits.

👉 Focus on:

- Budgeting

- Saving

- Investing

- Learning

Small steps taken today can lead to big financial success in the future.

FAQs

1. How much should I save in my 20s?

Try to save at least 20% of your income.

2. Is it necessary to invest in your 20s?

Yes, early investing helps you benefit from compounding.

3. Should I use a credit card in my 20s?

Yes, but only if used responsibly.

4. What is the biggest mistake people make in their 20s?

Not saving or investing early.

5. Do I need insurance in my 20s?

Yes, especially health insurance.